The ROI paradox.

Why bigger batteries are beginning to deliver better returns than smaller ones.

For years, the UK battery industry has operated on a relatively simple assumption: smaller batteries produce better ROI.The logic appeared sensible enough. Reduce upfront capex, shorten payback periods, minimise oversizing risk and keep proposals commercially digestible. Installers became conditioned to quote “the smallest battery that makes sense,” while customers became trained to ask one question above all others: “How quickly does it pay back?”

Historically, that mindset worked reasonably well because the battery itself was performing a fairly limited role. It was essentially a self-consumption device. Charge from solar during the day, discharge into evening demand, reduce imported electricity and hopefully achieve a decent payback period without spending too much money upfront.

It sounds counterintuitive at first. But once you understand how modern battery economics are evolving, the logic becomes difficult to ignore.

But the UK electricity system has changed dramatically. And increasingly, the economics of batteries are changing with it. Ironically, in many real-world commercial applications, larger batteries are now beginning to produce materially better long-term returns than smaller ones despite their higher upfront cost.

The spreadsheet battery

The smallest battery may no longer be the most profitable battery. To understand why this shift matters, it is important to understand how most battery systems were originally sized.

Historically, installers and consultants generally focused on three variables: annual electricity consumption, solar generation profile and evening demand. The goal was to maximise self-consumption while minimising unused battery capacity. If a customer only consumed 10 kWh overnight, then specifying a 30 kWh battery often appeared financially irrational. The “unused” capacity represented stranded capital and elongated payback.

This logic became deeply embedded throughout the industry. Spreadsheets rewarded smaller systems. Finance proposals rewarded smaller systems. Sales processes rewarded smaller systems. The entire market became optimised around capex minimisation.

But there was a hidden assumption underpinning all of this: that the battery’s future value would remain relatively static. That assumption no longer holds true.

The modern battery is no longer simply storing surplus solar energy. Increasingly, it is becoming a load-shifting device, a resilience asset, a peak-demand management tool, an EV charging buffer and, increasingly, part of a much wider operational energy system. That changes the equation entirely.

Once a battery begins performing multiple operational roles simultaneously, spare capacity stops looking wasteful and starts looking strategically valuable. A tightly sized battery may technically achieve a fast payback against today’s tariff structure, but it often lacks operational headroom. It becomes fully occupied servicing existing demand and therefore has very limited flexibility to participate in future opportunities. A larger battery, by contrast, may appear “too big” on day one, but earns its keep supporting the grid, and increasingly becomes more commercially useful on site over time.

The fictional factory

Imagine two manufacturing businesses with broadly similar operational profiles.

Business A installs a 1 MWh battery system.

Business B installs a 3 MWh battery system.

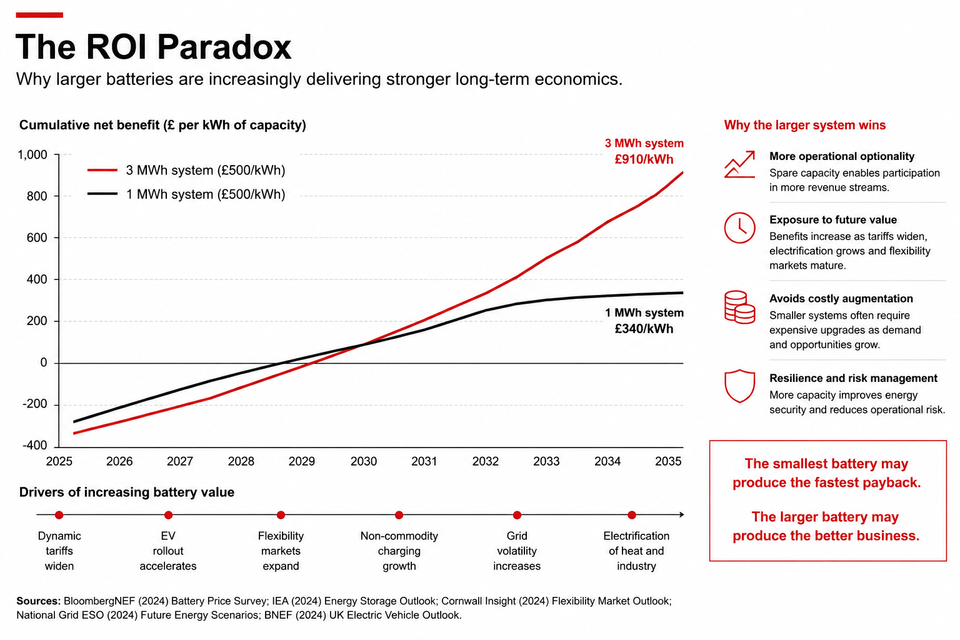

Both systems cost approximately £500/kWh installed. The 1 MWh system costs around £500,000, while the 3 MWh system costs approximately £1.5 million.

At first glance, the smaller battery appears financially safer. The payback model for the 1 MWh system looks attractive because the battery is heavily utilised from day one. Most of its capacity cycles daily against the site’s operational load profile. The 3 MWh battery, however, initially appears oversized. A large portion of its capacity remains unused during normal operations. Traditional ROI analysis would usually conclude the 1 MWh project is superior because the utilisation percentage appears higher and the initial payback looks cleaner.

But now fast-forward three years. Between 2026 and 2029 several things happen simultaneously across the UK electricity market.

Time-of-use spreads widen materially. Negative pricing events become more common due to excess renewable generation. The local DNO introduces stronger peak-demand charging structures. The business adds EV fleet charging. The site partially electrifies heating. Flexibility participation becomes easier through aggregation platforms. Capacity markets mature further. Electricity price volatility increases. Suddenly, the operational picture changes dramatically.

The 1 MWh battery is now constrained. It is already fully occupied servicing core operational demand. During high-value flexibility windows it often lacks spare capacity. EV charging increasingly competes with operational battery cycling. The system begins experiencing congestion between competing operational priorities. The business now faces an expensive decision: augmentation.

Additional switchgear may be required. Inverter limitations emerge. Site redesign becomes necessary. Installation disruption returns. Project mobilisation costs reappear. In practice, augmentation often costs materially more per incremental kWh than original deployment.

Meanwhile, the 3 MWh battery begins quietly outperforming expectations, because it retained operational headroom from the start. The larger system can absorb cheap overnight energy more aggressively. It can support larger peak-demand reduction windows. It can manage EV charging more effectively while still preserving reserve capacity. It can participate in flexibility events while simultaneously supporting operational loads. It can respond dynamically to changes in electricity pricing rather than simply reacting to static site demand.

Its utilisation profile improves over time as the wider electricity system evolves around it. Ironically, the battery that initially looked oversized becomes the battery producing materially stronger long-term returns.

Static ROI vs dynamic ROI

Traditional battery ROI models are largely static. They analyse the world as it exists today and assume relatively stable future operating conditions. But battery systems increasingly operate inside a highly dynamic electricity environment.

Read on: or hear this article read to you! Membership is free.

Electricity markets are becoming more volatile. Operational demand is becoming more electrified. Grid constraints are increasing. Flexibility services are expanding. Network charging structures are evolving. In that world, spare battery capacity increasingly behaves less like stranded capital and more like optionality.

The larger battery possesses more future pathways to monetisation. That does not guarantee success, of course. Oversizing irresponsibly can still destroy project economics. But the historical industry instinct toward aggressively minimising system size is becoming increasingly questionable, particularly in commercial environments where electricity demand itself is evolving rapidly.

This is where many older battery-sizing assumptions begin to look dangerously simplistic, because the original spreadsheet models were built for a different electricity market entirely.

Commercial energy is becoming operational

This shift is particularly important in commercial and industrial environments because commercial electricity costs are becoming increasingly operational in nature.

Historically, many businesses focused almost entirely on total electricity consumption. Increasingly, however, businesses are being exposed to peak-demand charging, DUoS exposure, non-commodity charging, operational load volatility, EV charging demand and resilience requirements.

A battery is no longer simply offsetting imported electricity. It is increasingly reshaping how the business interacts with the electricity system itself. A larger battery therefore often creates disproportionately larger operational value because it can influence when electricity is consumed, how sharply demand spikes occur, how EV charging is managed and how the site behaves during periods of network stress.

This is one reason sophisticated commercial operators are beginning to think operationally rather than simply electrically: The battery increasingly becomes infrastructure.

The flexibility layer

The biggest long-term wildcard remains flexibility markets. Most batteries installed historically were never designed with flexibility participation in mind. They were sized almost entirely around self-consumption. But aggregated flexibility increasingly changes battery economics because larger batteries generally provide more 'dispatchable' spare capacity.

A battery fully occupied servicing overnight demand contributes very little flexibility to the wider system. A larger battery with operational reserve capacity can increasingly respond dynamically to external market signals. This is where Virtual Power Plant economics begin emerging.

And importantly, flexibility value often scales non-linearly with capacity. The larger battery does not simply create more storage. It creates more operational freedom. That operational freedom increasingly becomes monetisable through dynamic tariffs, flexibility participation, peak-demand management and increasingly sophisticated aggregation models. This is one reason the next generation of battery economics may look materially different from the previous one.

Historically, installers were rewarded for minimising system size. Increasingly, they may be rewarded for intelligently future-proofing operational capability instead.

The installer opportunity

This shift creates a major opportunity for installers willing to rethink how they approach specification conversations. Historically, many installers have understandably focused on fastest payback because it simplified the sales process. But increasingly, customers need help understanding how their electricity usage may evolve over the next decade.

That conversation now includes EV charging, electrified heating, operational resilience, flexibility participation, dynamic tariffs, peak-demand management and future operational expansion. Installers who understand this transition early may naturally begin specifying differently from competitors still focused entirely on capex minimisation.

The conversation becomes less “What is the cheapest battery we can justify?” and more “What operational capability might this site eventually require?” That is a much more strategic discussion, and increasingly it may produce much larger project values.

The next phase of battery economics

None of this means bigger batteries are always better. Poorly specified oversizing remains dangerous. But the simplistic industry assumption that smaller automatically equals better ROI is beginning to look increasingly outdated.

Because battery value is no longer created purely through self-consumption: It is increasingly created through operational flexibility, resilience, dynamic optimisation, load management, future electrification readiness and participation in increasingly complex electricity markets. The irony is that the battery which initially looks too large on today’s spreadsheet may ultimately become the battery with the strongest economics five years later.

That is the ROI paradox.

And as the UK electricity system becomes more dynamic, more volatile and more operationally complex, it is likely to become one of the defining commercial realities of the next generation of battery storage.

Member discussion